Insights

The widening confrontation between the United States, Israel and Iran has rapidly evolved from a geopolitical flashpoint into a material macroeconomic risk. For investors, the key transmission mechanism is clear: energy.

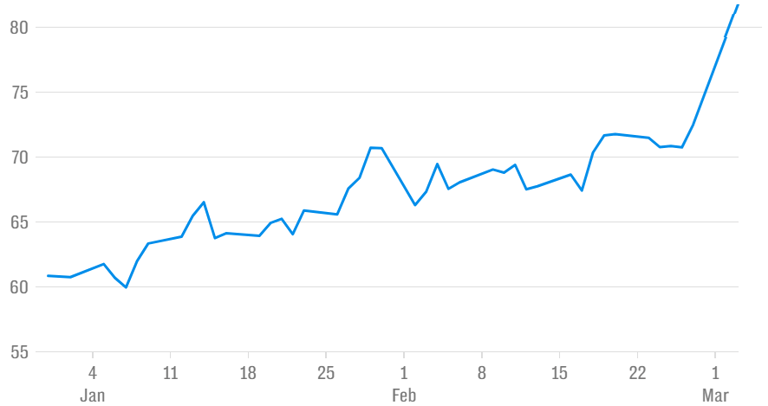

Brent crude has climbed to $82 a barrel, while European natural gas prices have surged to levels not seen for months. At the same time, equity markets have sold off sharply and bond yields have risen as traders reassess the trajectory for inflation and monetary policy. What had been a relatively constructive backdrop for risk assets now looks more fragile.

Brent Crude price per barrel

$

War in Middle East Rattles Markets

3rd March 2026

Andrew Morgan, CFA

Portfolio Manager

_________________________________________________

Source: Bloomberg

Energy supply: the central variable

The Strait of Hormuz remains the focal point for markets. Roughly a fifth of global oil supply passes through this narrow shipping corridor along Iran’s southern coast. With commercial shipping activity reduced and insurers repricing risk, the effective supply of oil and gas from the Gulf has tightened even without a formal blockade.

Brent’s move to $82 reflects both physical disruption and risk premium. In isolation, that price level is not historically extreme. However, the pace of the rise – combined with the simultaneous spike in gas – has unsettled investors who had been positioned for a benign disinflationary environment.

The more acute development has been in liquefied natural gas. Following Iranian strikes on energy infrastructure in Qatar, QatarEnergy has halted production at key facilities. Given that Qatar accounts for roughly 20 per cent of global LNG supply, the implications are significant. Europe’s benchmark TTF gas price has jumped sharply to €56.5 per megawatt hour, intensifying competition between European and Asian buyers for cargoes.

In short, energy markets are repricing a higher probability of sustained supply constraint rather than a short-lived disruption.

From growth scare to stagflation risk

The market reaction has been swift and broad-based. European equities have led the decline, with the Stoxx Europe 600 suffering its steepest daily fall since last year’s tariff-related volatility. Germany’s Dax has dropped heavily, here in the UK the FTSE 100 was down 2.6 per cent at the time of writing, and US futures indicate further weakness in the S&P 500 and Nasdaq 100. Investors are moving to reduce cyclical exposure and reassess earnings assumptions under a higher-input-cost regime.

The concern is not simply slower growth, but the re-emergence of stagflation risk: weaker economic activity alongside renewed price pressure.

Oil at $82 is unlikely, by itself, to derail the global expansion. Historically, economists estimate that each sustained $10 rise in oil subtracts roughly 0.1–0.2 percentage points from global growth over the following year. However, if crude were to extend decisively higher – potentially breaching $100 – the impact would become more pronounced.

More importantly for markets, the direction of travel for inflation expectations has shifted.

Central banks forced to reconsider

Bond markets have responded by pushing yields higher, especially at the front end of curves. In the euro area, traders are now assigning a meaningful probability to a rate increase by the European Central Bank before year-end — a notable reversal from earlier expectations of further easing. Two-year Bund yields have climbed accordingly.

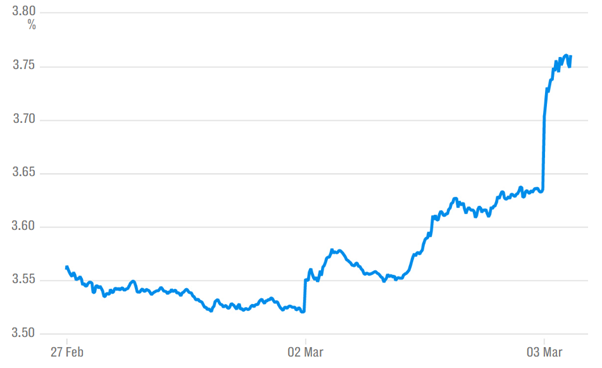

In the UK, the repricing has been equally stark. The likelihood of a near-term cut by the Bank of England has fallen sharply, with markets now anticipating a slower pace of policy easing. Two-year gilt yields have risen as investors reassess the balance of risks facing the Monetary Policy Committee.

Two-year gilt yield

Source: Bloomberg

Across the Atlantic, US Treasuries have also sold off. Although the United States is far more energy self-sufficient than in previous decades, domestic fuel prices are still determined by global benchmarks. A sustained rise in crude complicates the calculus for the Federal Reserve, particularly if higher petrol prices begin to filter into inflation expectations.

For policymakers, the dilemma is familiar: whether to “look through” an externally driven energy shock or respond pre-emptively to prevent second-round effects. For investors, the practical implication is that the path to rate cuts has become less certain.

Regional exposure: uneven but meaningful

Asia is structurally exposed to Gulf energy flows. The majority of crude and condensate transiting the Strait of Hormuz is destined for Asian economies, including China, India, Japan and South Korea. For China in particular, higher import costs risk compounding existing domestic headwinds and weighing on industrial margins.

Europe’s vulnerability lies in gas. Since the sharp reduction in Russian pipeline supply, LNG has become a critical marginal source of energy. Disruption in Qatari exports tightens an already competitive market and raises the prospect of renewed pressure on household and industrial energy bills.

For both regions, the macro impact depends on duration. A short-lived spike can be absorbed. A sustained elevation in prices, however, would have more durable consequences for consumption, corporate profitability and fiscal balances.

Currency and cross-asset implications

Geopolitical shocks of this nature have historically supported the US dollar, as investors rotate towards perceived safe-haven assets. A firmer dollar, in turn, tightens financial conditions globally, particularly for emerging markets with dollar-denominated liabilities.

Credit markets are also vulnerable. Higher input costs erode margins, particularly in energy-intensive sectors, while rising front-end yields reduce the appeal of longer-duration risk assets. The recent weakness in equities and government bonds reflects a broad recalibration rather than a narrow sectoral adjustment.

What to watch from here

For investors and clients, the key variables over the coming weeks are clear:

Shipping flows through the Strait of Hormuz – Any sustained impairment would materially increase the probability of oil testing higher levels.

The durability of the LNG disruption – Qatar’s production decisions will be critical for European and Asian gas markets.

Inflation expectations – Breakevens and survey data will indicate whether energy is feeding into broader pricing behaviour.

Central bank communication – Guidance from the Federal Reserve, the European Central Bank and the Bank of England will shape rate expectations and cross-asset performance.

At $82, oil is a warning signal rather than a crisis threshold. But markets are forward-looking, and the current repricing reflects concern that this conflict may prove more persistent and economically disruptive than initially assumed.

The global economy has shown resilience in the face of multiple shocks over the past year. Whether that resilience endures will depend less on headlines and more on the trajectory of energy supply. For now, volatility is likely to remain elevated.

Our Positioning

Our portfolios were already relatively defensively positioned. Our largest equity holding is the First Trust US Buffer fund – a defensive fund that protects on the downside while participating in most of the upside. Gold also serves as a safe haven during volatile times; we expect continued outperformance of the gold fund we hold in most client portfolios. In response to the unfolding events in the Middle East, we have thought it prudent to increase the defensiveness of client portfolios. As a result, we have modestly reduced our equity exposure, whilst increasing short-duration bonds.