The Weekly Note

Global markets remained resilient as robust US corporate earnings and strong Japanese wage data offset geopolitical jitters. While the US labour market showed continued strength, European sentiment was tempered by hawkish ECB rhetoric and renewed tariff threats. Overall, AI-driven tech momentum continues to underpin growth despite cautious consumer sentiment.

United States

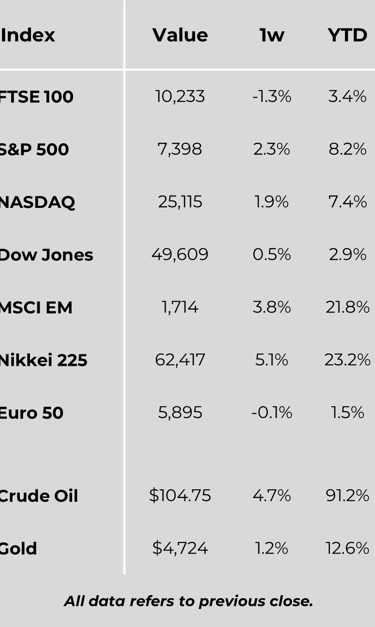

US equity markets rallied this week, underpinned by a robust corporate earnings season. With 85% of the S&P 500 having reported, nearly 85% of those firms exceeded consensus estimates, delivering an aggregate earnings surprise of 19%. The technology sector led the charge, fuelled by sustained momentum in artificial intelligence (AI) infrastructure. In contrast, the energy and utilities sectors lagged behind.

The labour market continues to show resilience; new unemployment claims fell below expectations at 200,000, while continuing claims hit their lowest level since 2024. Non-farm payrolls also impressed, adding 115,000 jobs in April—significantly ahead of the 62,000 forecast. Despite this strength, the participation rate fell to its lowest since late 2021, and tech layoffs increased as firms pivot toward AI-driven efficiencies. Elsewhere, construction spending and factory orders both beat expectations, driven by housing projects and electronics demand. Conversely, consumer sentiment tumbled to a record low, hampered by concerns over fuel prices and potential tariffs.

Europe

The STOXX Europe 600 ended a volatile week with modest gains. Sentiment was initially buoyed by easing Middle Eastern tensions, but optimism was tempered later by renewed US rhetoric regarding potential trade tariffs. Regional performance was mixed; Italy’s FTSE MIB rose over 2%, while the UK’s FTSE 100 fell 1.26% following the Easter Monday bank holiday.

Monetary policy remains a focal point, with the ECB signalling a potential June rate hike unless inflation shows a "substantial and sustained" improvement. This hawkish stance follows news that eurozone producer price inflation rose 3.4% in March—the largest monthly jump since 2022—largely due to surging energy costs. In manufacturing, German factory orders surged by 5.0%, far exceeding forecasts, though the country's construction sector remains in a sharp downturn. More positively, the UK Composite PMI rose to 52.6, indicating a healthy expansion across both manufacturing and services.

Japan

Despite being closed for much of the week for the Golden Week holiday, Japanese markets surged upon reopening. The Nikkei 225 reached a record high, gaining over 5% on AI-related tech enthusiasm and hopes for easing geopolitical tensions. Falling oil prices provided further relief for the energy-import dependent economy. Notably, real wages rose for the third consecutive month—the first such streak since 2021—suggesting a durable wage-price cycle that may allow the Bank of Japan to continue normalising monetary policy.

China

Chinese markets advanced as investors returned from the May Day break. The CSI 300 and Hang Seng indices both gained, supported by resilient domestic demand and preparations for the upcoming Trump-Xi summit. While services activity expanded at a faster pace in April, holiday travel data revealed a nuanced picture; although trip volumes rose, spending per head declined slightly, suggesting that consumers remain cautious regarding discretionary expenditure.

Other Key Markets

In Romania, markets navigated political instability following the removal of the government. While the leu hit record lows, stocks recovered late in the week as fiscal data came in better than expected. In Colombia, the central bank surprised markets by holding interest rates at 11.25%. A hawkish tone, combined with fiscal uncertainty ahead of the May presidential election, led investors to price out near-term easing.

Major Company News:

HSBC reported a first-quarter profit of $10.1 billion. While earnings per share fell short of some forecasts, the bank’s revenue rose 6%, driven by strong wealth management fees and higher interest income. Consequently, they upgraded their full-year income guidance to $46 billion.

Toyota announced record annual revenues of 50.7 trillion yen ($336 billion), supported by a 5.5% increase in vehicle sales. Despite this top-line growth, operating income dipped as the firm ramped up investments in battery-electric and hydrogen technology to maintain its global leadership.

Shell reported robust first-quarter results, buoyed by volatile energy prices and its strategic acquisition of ARC Resources. The energy giant continues to simplify its executive structure and remains focused on shareholder returns through its steady quarterly dividend and buy-back programmes.

The CEOs of ASML, SAP, and Airbus issued a joint "wake-up call" to EU policymakers. They called for urgent reforms to competition rules and increased R&D support, warning that fragmented European markets are losing their global technological edge to US and Chinese rivals.

Chinese EV giant BYD projected annual sales of up to 5.5 million units for 2026, a 20% increase. The company is aggressively expanding its overseas footprint, with new models and ultra-fast charging technology helping it defy a general cooling in domestic electric vehicle demand.

11th May 2026

_____________________________________________________________